Despite being touted as a pro–working-class policy that spurs economic activity, sales tax holidays fail to increase economic growth while imposing burdensome compliance costs on small businesses and disproportionately benefiting affluent individuals.

From 2002 through 2013, North Carolina offered a back-to-school sales tax holiday during the first weekend in August, for which eligible items, such as school supplies and clothing, were exempt from the sales tax. While it might sound like an effective method of boosting the economy and providing tax relief to hardworking families, in practice the sales tax holiday was more of a symbolic gesture than a substantive fiscal policy measure.

Interestingly, NC House policymakers have proposed reinstating the back-to-school sales tax holiday in their recent budget, despite the state’s sustained economic success over the past 12 years without the policy.

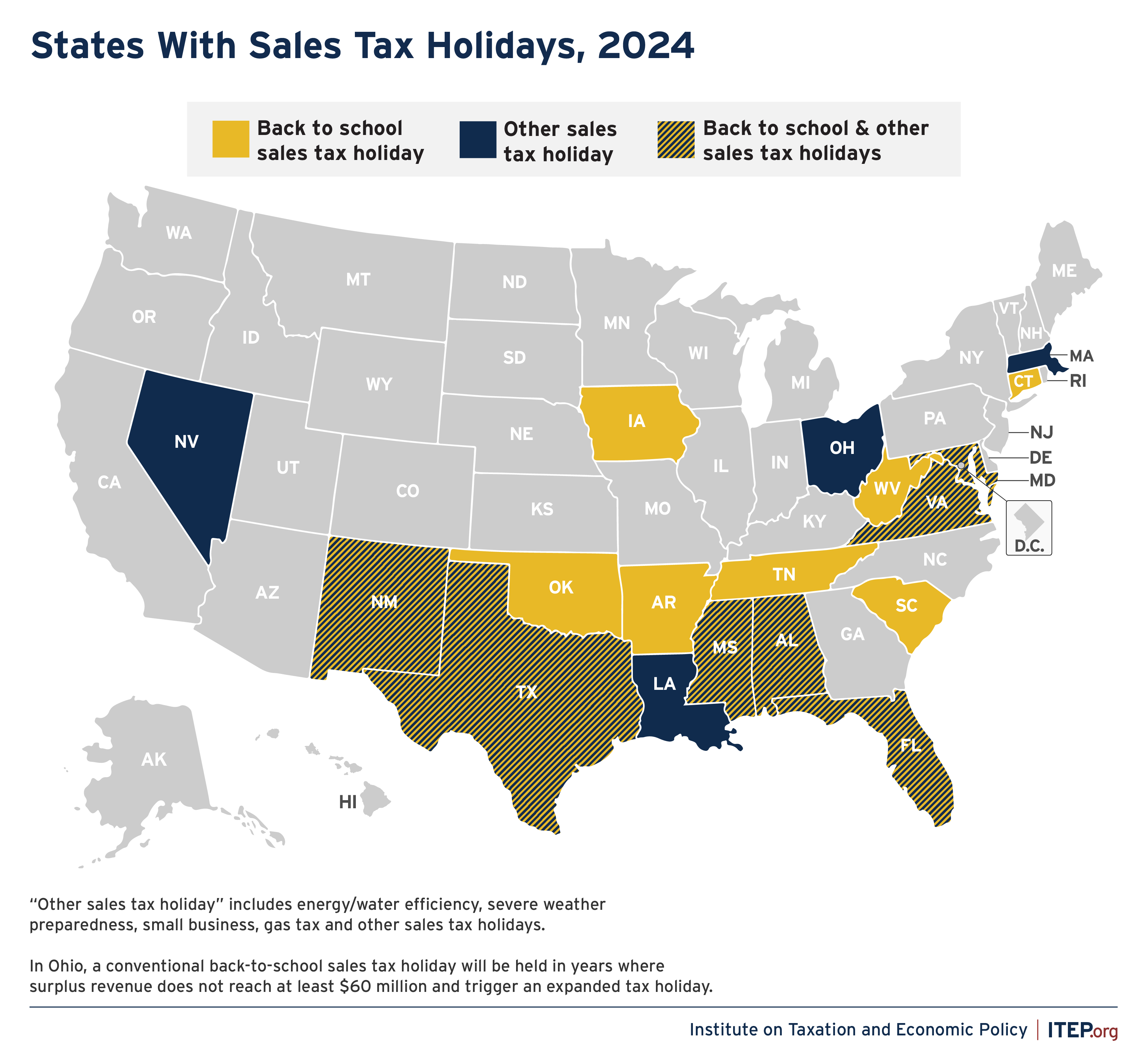

Sales tax holidays are time-limited tax exemptions that target specific categories of goods. Nineteen states currently offer some form of sales tax holiday. The holidays range from recreational equipment to hunting gear to severe weather preparedness supplies. However, the vast majority focus on education-related items and clothing, known as back-to-school sales tax holidays.

Back-to-school sales tax holidays are particularly popular because they invoke powerful emotional images. Think of working-class parents being able to buy all the items on their son’s fifth-grade supply list, or a struggling single mom being able to buy her daughter the shoes she needs for preschool. Such stories tug on our heartstrings. Nevertheless, policies should be measured by their results rather than their intentions.

Sales tax holidays appear to offer meaningful benefits to consumers and the state, but in reality they pick winners and losers and shift the timing of purchases without increasing their volume. Rather than generating new economic activity, sales tax holidays incentivize consumers to delay or fast-forward already planned purchases to take advantage of the perceived discount. Consequently, the holidays are suboptimal policies relative to broad permanent tax cuts that generate lasting growth by incentivizing new economic activity.

Moreover, affluent individuals have a much greater capacity to adjust the timing of purchases, which allows them to capitalize on the tax holiday more easily due to having greater savings and disposable income.

For example, a wealthy couple could take advantage of the back-to-school sales tax holiday by purchasing two $3,000 computers, two $200 printers, and 10 items of clothing each valued at $80. At the Wake County sales tax rate of 7.25%, this would save the affluent couple $522. Meanwhile, the working-class parents who spend $100 on their son’s school supplies would save $7.25, and the single mom would save only about half of that on her daughter’s shoes — if they time their purchases to take advantage of the short, tax-free window.

Sales tax holidays also increase business compliance costs by requiring accurate identification of eligible products and proper cash register updating. While these changes might be relatively easy for a large corporation, they can be particularly burdensome to small businesses that operate with limited resources. For these businesses, properly implementing the holiday can be costly and disruptive.

Additionally, sales tax holidays predictably induce temporary increases in demand that can result in market shortages for eligible products. Savvy retailers are able to anticipate the surge in demand and increase prices accordingly. As a result, the intended tax savings for consumers can be partially — or even entirely — offset by higher prices. In many cases, consumers are unaware that their savings have been reduced or erased, undermining the effectiveness of the policy and distorting its perceived benefit.

Finally, sales tax holidays may also signal a broader issue: namely, that the regular sales tax is so burdensome that it justifies temporary relief.

Sales tax holidays are flashy but flawed fiscal policy tools. They are often embraced for the emotional comfort they provide rather than the economic value they deliver. In reality, sales tax holidays sacrifice the opportunity for more broad-based cuts that would grow the economy, impose unnecessary burdens on small businesses, and disproportionately benefit people with large amounts of disposable income, not those living paycheck to paycheck.

{kind=link}